There has been a regime change: TINA is hobbling.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

There has been a regime change: TINA is hobbling.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Listen to the The Macro Trading Floor Podcast

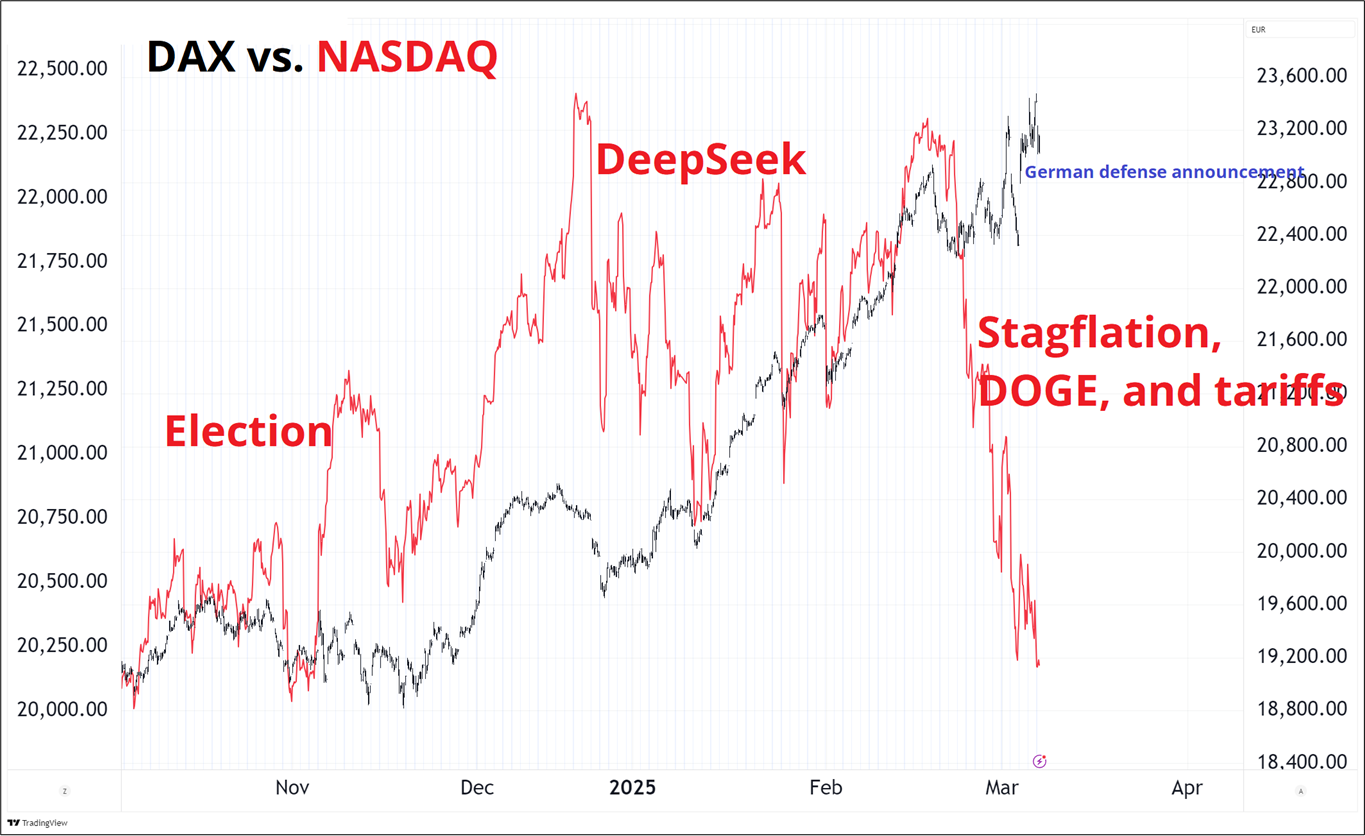

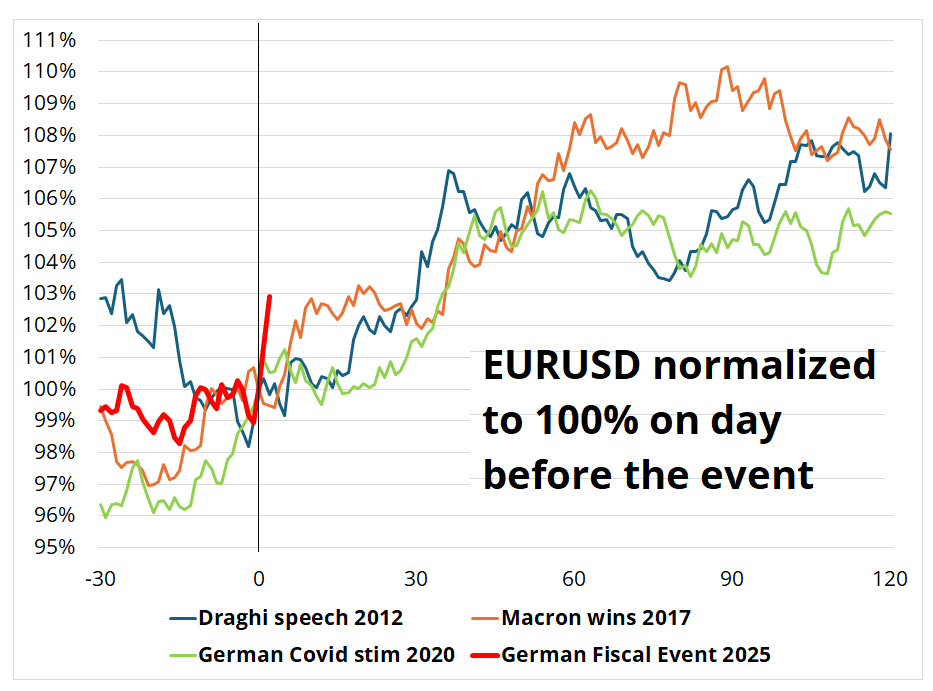

Another cacophonous week of badly-confused and poorly-planned US policy rollout was trumped by a massive announcement out of Germany as they announced a gigantic defense spending plan. Germany will spend more than 10% of GDP on defense and infrastructure over the next 10 years in a removal of the debt brake. This is a regime change for global macro.

The new regime brings a weaker USD, stronger EUR, and massive outperformance of global equities vs. the US as the years-long theme of American Exceptionalism has turned on a dime to “anything but the USA.” Peak AI capex fears on top of paralyzing uncertainty over bungled tariff rollouts, not to mention stagflation fears, a weakening US jobs market, and a foreign exodus from US stocks have all flipped the script almost overnight.

In an amazing reversal, we went from TINA (there is no alternative to the US), China is uninvestable, and Europe is dead… To a market that is fleeing anything made in the USA and looking for safer places to park cash.

The China NPC is meeting into next Tuesday, and so we await post-COVID stimulus announcement number 642.

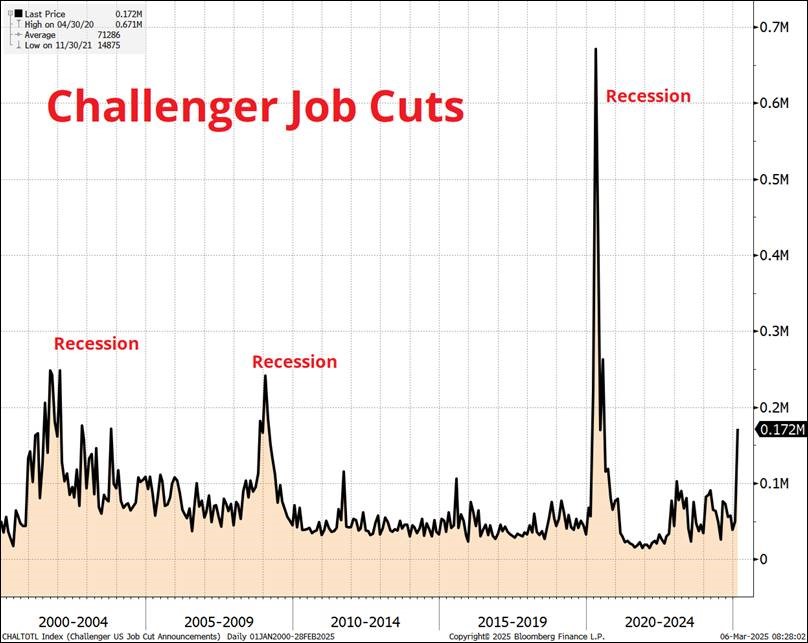

The US jobs report was OK today, but there are warning signs:

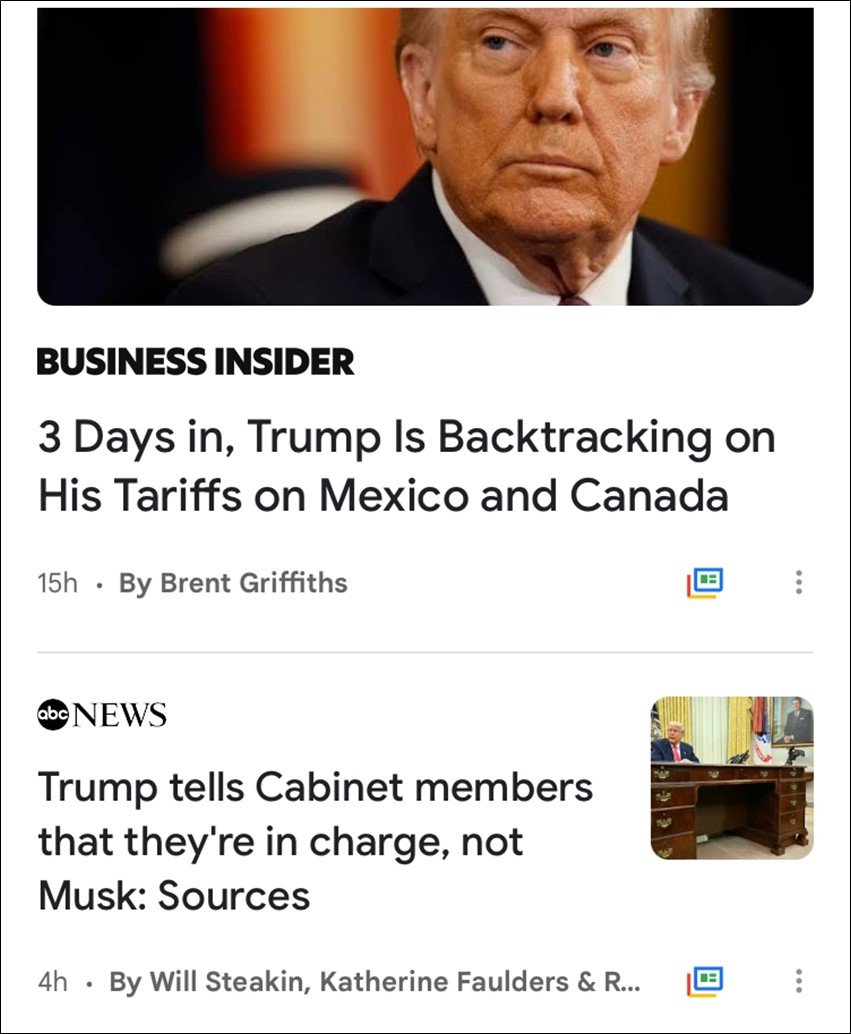

As the policy vibe remains confused and backtracky.

As shown above, US equities are getting smashed as confidence flipped from all-time bullish after the election to nearly record bearish of late. The market got the election wrong and now everything has pretty much reverted to the mean. It seems like the US administration is front-loading most of the bad news (job cuts, inflationary immigration policy, tariffs, etc.) while the good news (tax cuts and deregulation) will take longer to play out.

There is an argument that tariffs are not necessarily bearish if executed professionally with some clarity, but when they are on and off, up and down, and across-the-board and then targeted, the uncertainty freezes investment and hiring because businesses don’t know the rules of the game and therefore must back away and wait for clarity. The big-ticket numbers for Stargate and other government efforts are offset by policy paralysis. While companies might in theory move production to the US to avoid tariffs, they also might want to know what the tariffs actually are before doing so.

The market is also getting the sense there is no real plan as Trump announces something, then stocks fall, and then they roll out Lutnick to reverse whatever Trump said. When the dust finally settles on policy, risky assets should stabilize. Until then, the market has no way of gauging policy impact and would rather reduce allocations to the US until the administration gets organized.

My guess is that foreign sovereign holders of US equities are also dumping while they still can as the risk of some kind of tax on foreign holders looms large. If you’re China Investment Corp. or a sovereign wealth fund and you have a grillion dollars of US equities and you think there’s even a tiny chance they might be arbitrarily taxed in the future, you probably want to lower your allocation or risk being fired (or worse).

From NYU Law Review:

Sovereign wealth funds enjoy an exemption from tax under § 892 of the tax code. This anachronistic provision offers an unconditional tax exemption when a foreign sovereign earns income from noncommercial activities in the United States. The Treasury regulations accompanying § 892 define noncommercial activity broadly, encompassing both traditional portfolio investing and more aggressive, strategic equity investments. The tax exemption, which was first enacted in 1917, reflects an expansive view of the international law doctrine of sovereign immunity that the United States (and other countries) discarded fifty years ago in other contexts.

And here’s an article from a few weeks ago by a Columbia tax law professor and a senior fellow from the Council on Foreign Relations.

https://www.foreignaffairs.com/united-states/better-tool-counter-chinas-unfair-trade-practices

This week’s 14-word stock market summary:

There is a new kid in Equity Town. Her name is Europe, not TINA.

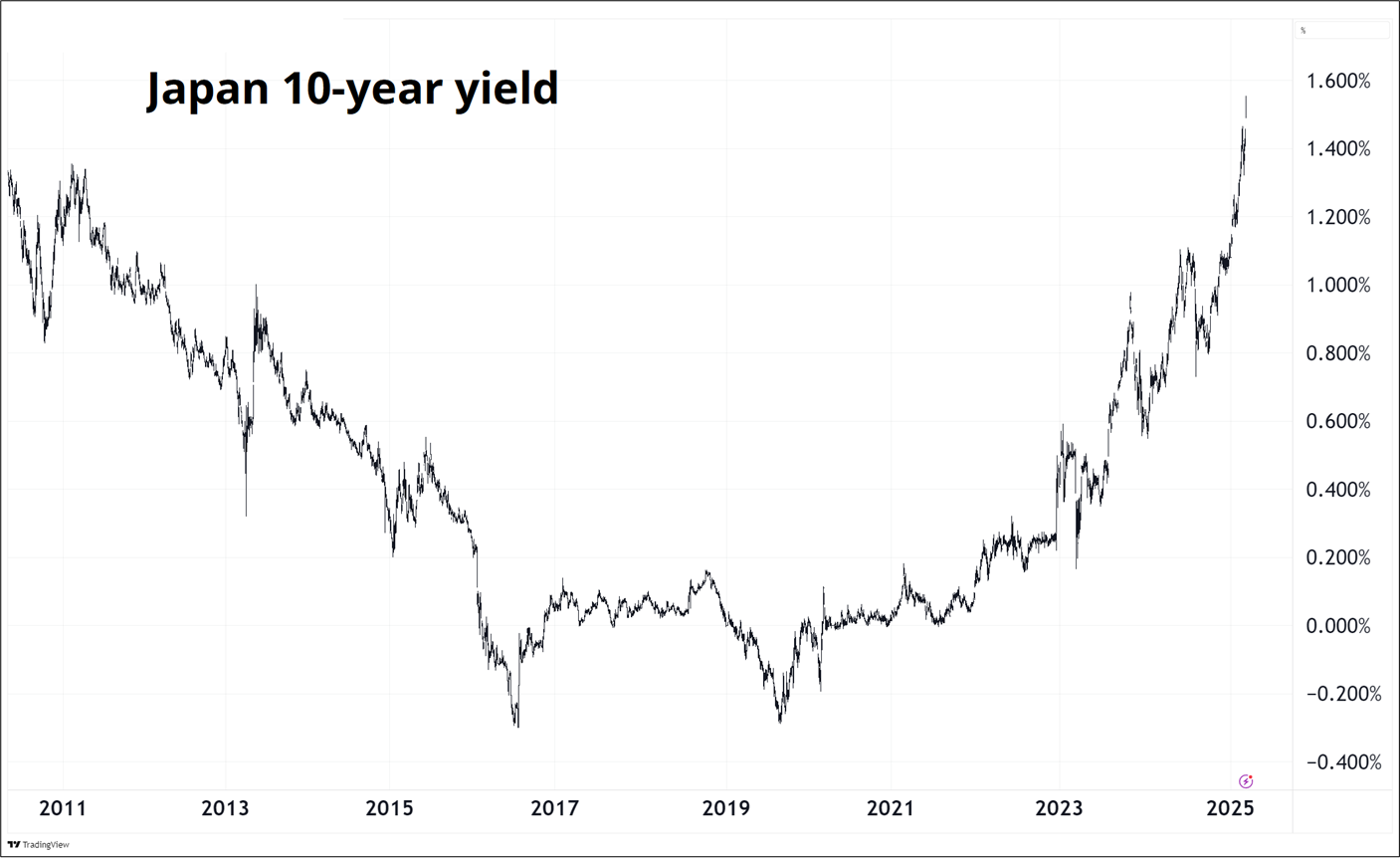

German yields had their largest move since the fall of the Berlin Wall. That’s the story in rates this week and everything else is a sideshow.

This move was a direct response to the rapid opening of the fiscal floodgates in Europe. It’s not just the size of the spending program that caught the market off guard, the speed with which they are doing this is also mind-blowing. Europe as the slow, plodding bureaucracy was upended a bit here as the Germans are jamming through a monster policy change before the new Bundestag can sit down. Impressive!

Japanese government bonds (JGBs) also joined the party and yields in Japan are making fresh post-GFC highs. I have a gut feeling that this is going to be the highs in Japanese yields as demand from Japanese pension funds will likely emerge above the 1.5% yield level and we will start to see repatriation out of foreign bonds and into JGBs. Funding Japan’s mega debt pile is getting too expensive.

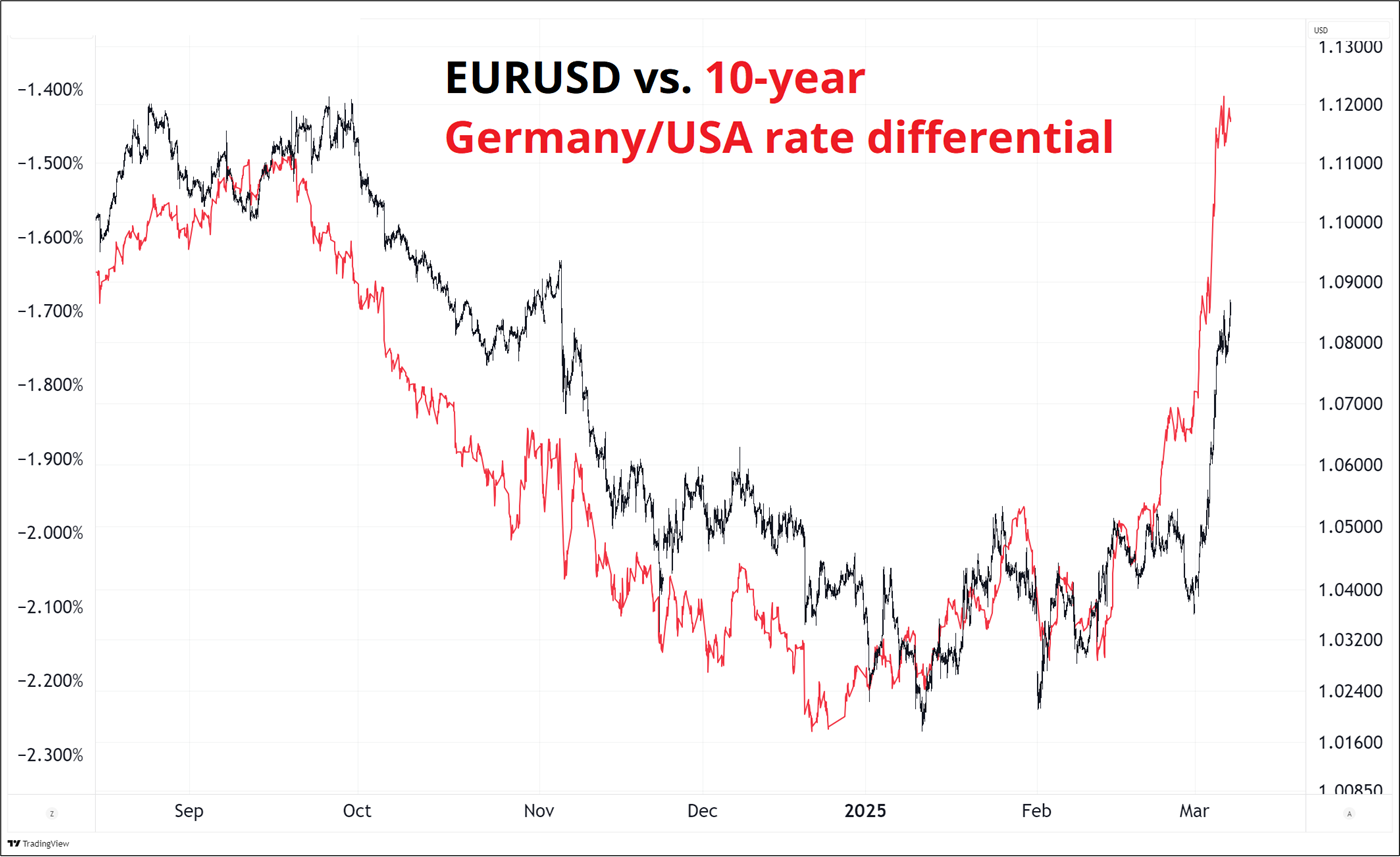

The first clue that the USD was toast was when Trump’s 25% tariff on Canada came in and USDCAD did not go up. The market was expecting a massive spike in USDCAD, and instead, it popped about 30 points then fell 200. When something weird like this happens in the market, it’s always worth paying attention. This was enough of a tell for me that I went long EURUSD in am/FX on Tuesday in response. If one USD pair isn’t going to react to tariffs, you know others probably won’t either, and the short euro trade was partly predicated on tariff risks. Also, interest rate differentials, which often lead FX markets, were already pointing to much higher EURUSD.

Note how the red line (rate diffs) moved down before EURUSD turned in October 2024 and then ripped higher before EURUSD turned higher this month. It’s never easy but interest rate differentials are almost always the number one driver of G10 FX. Trading the lead/lag relationship is an art and a skill and can be extremely rewarding but also sometimes sad-making. It doesn’t work 100% of the time, obviously, and when it doesn’t work, it’s very hard to know when to give up.

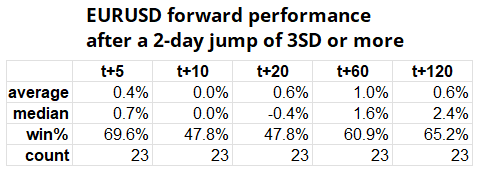

For the dollar, it feels pretty safe to say we are in a regime change here. The US has gone from exceptional to questionable while the EU and China have gone from uninvestable to raging. As I said above, Wednesday’s move in German yields was the biggest since 1990, and the 2-day move in EURUSD was greater than four standard deviations.

Editor’s note: Some people dislike the usage of the term “standard deviation” in financial markets because standard deviation is a term designed for describing normally-distributed data. Everyone knows that financial market data is not normally distributed (if you don’t, read up on it—it’s important!) … So we use standard deviation as a heuristic to easily describe the size of a move, even though we know that technically it’s not the best way to describe data with fat tails. It’s a shorthand that financial market professionals understand, even if it’s not perfectly on fleek for mathy quants.

While garden variety overbought is often a good play for mean reversion, impulsive, explosive moves like this EURUSD move are not fades. Here’s the data:

You can see after a mega move, EURUSD keeps going. It’s a tell that the market is the wrong way. This is an important aspect of overbought that people don’t consider thoughtfully enough. When nothing is going on, and the thing gets overbought, sell it. When there is a regime change and the thing gets overbought, buy dips.

As someone with a strong bias towards mean reversion and buy low / sell high strategies, I learned this lesson the hard way. Overbought and oversold are regime sensitive indicators. In a strong trending macro regime, overbought is a signal of a strong trend.

An interesting thread running through the current narrative is a bit intellectual and structural for my liking, but still bears mentioning. This meme is a good heuristic to begin with it. The USD isn’t backed by nothing.

The implication is that US hegemony is partly a military thing. By acting as World Police and defender of the Rules Based Order (RBO), the US made its currency a symbol of neocon/neoliberal RBO supremacy. The US pivot away from this global philosophy and towards lower defense spending mildly reduces that feeling of unassailable American hegemony. Meanwhile, Europe is stepping in to fill the gap, so the consensus prior that Europe is a milquetoast, bureaucratic, and declining power gets a bit of an asterisk now and maybe that’s good for a small change in the perceived value of the USD vs. the EUR as a reserve currency? Again, this is ivory tower intellectual stuff—not a tradable thesis, but also not completely nonsensical.

Ultimately, my bullish EURUSD view rests more on interest rate differentials and the massive outperformance of EU equities, and less on the bigger picture geopolitical stuff which can often be interpreted whatever way your confirmation bias decides. One could easily argue that less military spending is good for the US deficit situation and will eventually be good for the dollar. But I won’t argue that right now because I’m bearish dollar. :]

It is probably no coincidence that MAG7 earnings growth peaked, DeepSeek freaked everyone out, and the AI bubble got deflated at the same time as the USD peaked. It is reminiscent of 1999/2000, when a torrent of money flooded into the US and the USD became mega overvalued. Then, the money flowed out and the USD sold off throughout 2003, 2004, 2006, and 2007. 2005 was an exception due to repatriation related to the Homeland Investment Act. I’m not calling a 3-year bear market for the USD, but if you did, you could probably argue it pretty well.

Note that the USD peaked way, way after dotcom because that was the period right after the hatching of the EUR and the market was questioning whether the EUR was a soft currency like ESP, FRF, ITL or a hard currency like DEM. The low in EURUSD was put in by central bank intervention and then the BIG TWIN DEFICITS trade rocked and rolled as central banks diversified out of USD and into EUR, GBP, and everything else. This time, there is no such problem with the EUR. It’s cheap, and there will be plenty of fixed income assets to invest in as Germany will be issuing like mad.

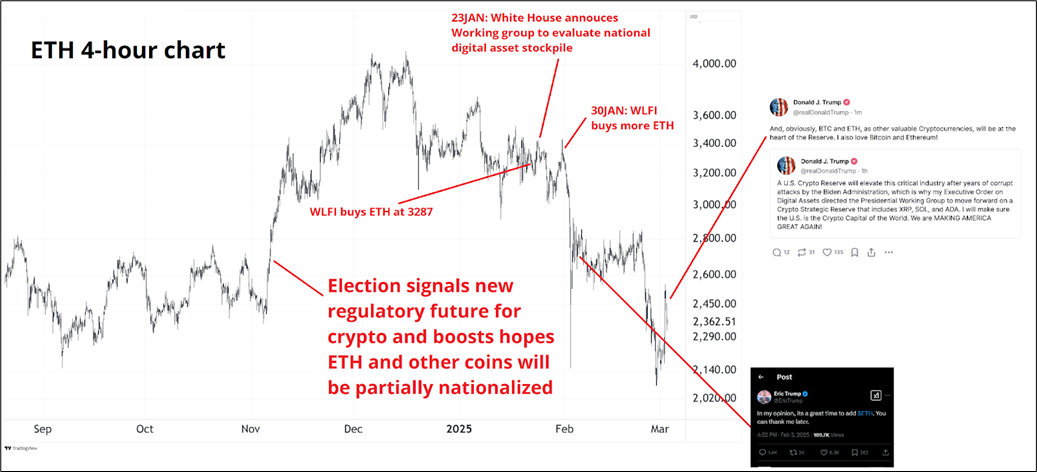

There was a crypto summit and they decided to keep the existing coins but not buy any new ones for now. The anger and vitriol in response to the idea of purchasing BTC, ETH, ADA, XRP, and SOL in the open market was too much even for the owner of $TRUMPCOIN to deal with and so it looks like they are backing away from the appalling idea of buying crypto with taxpayer money. Diverting funds from foreign aid and veteran’s affairs into Cardano was too much, even for the most hearty crypto natives.

That Reddit post sounds logical enough, though there is a different reason to forecast the death of crypto every year and I guess this is the latest one? Much as the use case / bull argument shapeshifts every year (It’s a currency! It’s decentralized! It’s a store of value! It’s a tech stock! It’s a—cough—the government is gonna buy it!) the apocalypse is always coming too (It’s a Ponzi! It’s only used for doing the crimes! FTX is Crypto’s Downfall!)

If you’re not hysterically bullish or bearish crypto… You’re not trying hard enough.

The Trump pump and dump is hitting diminishing returns:

Crude oil continues to break hearts in both directions and we are back to the bottom of the range. The most interesting feature of the crude market these days is how it’s having zero impact on macro. Bonds, USDCAD, and MXN barely even watch oil anymore, whereas there have been regimes when oil was all that mattered for macro. The reordering of the global oil market, the stable and low inflation-adjusted prices of oil and gasoline, and the end of US reliance on foreign crude have all conspired to reduce the relevance of the price of oil on a day-to-day basis.

I keep waiting for gold to release to the downside, but it can’t. It peaked in mid-February and made a spicy attempt to break lower, but has now mostly recovered. The moving averages are starting to turn higher and my short gold view is getting stale. Here’s the hourly chart.

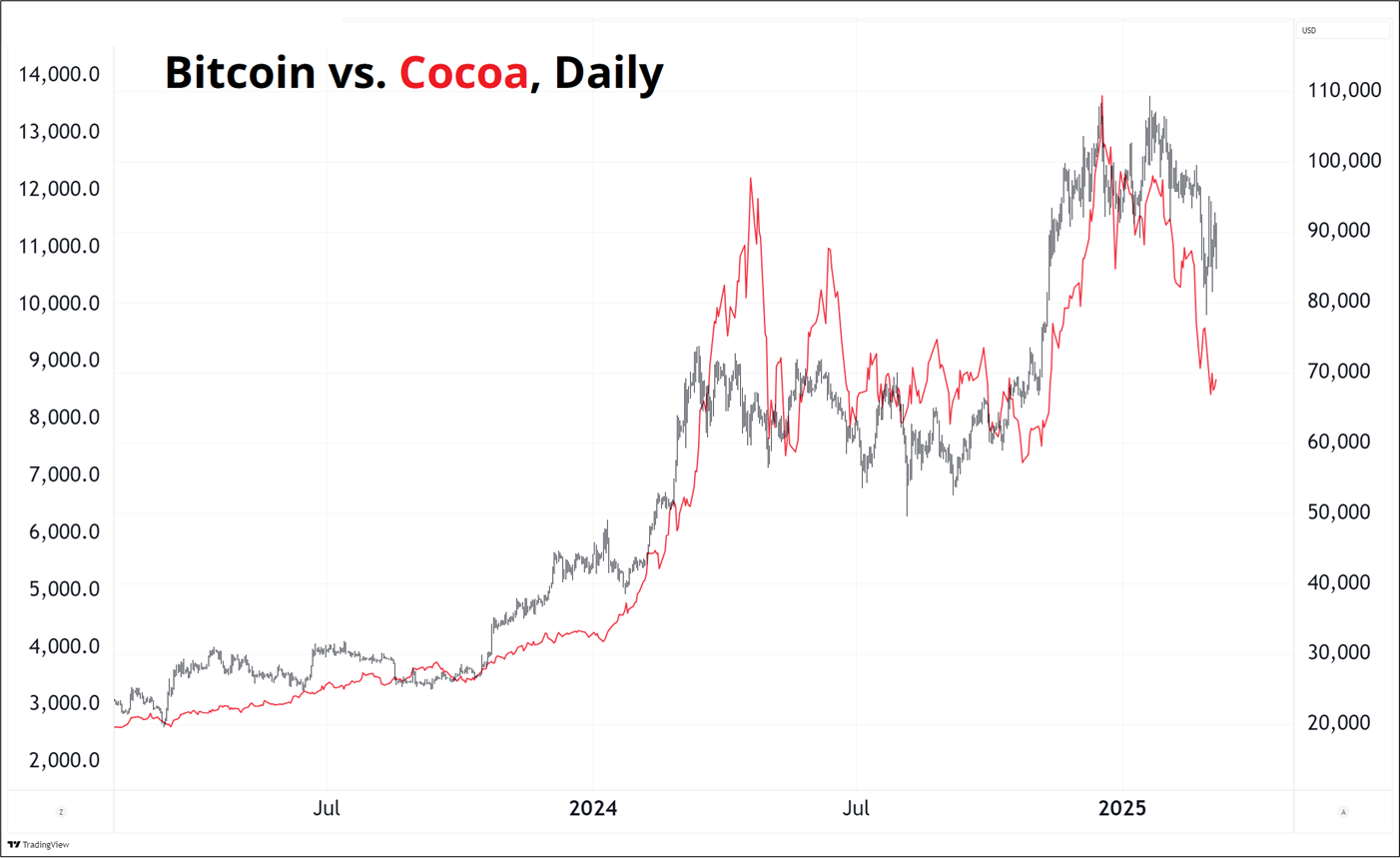

And in case you don’t follow them, the air has come out of the ags, finally. Here’s cocoa, a chart which looks suspiciously similar to a chart of TSLA or BTC. It’s almost as if these speculative moves have nothing to do with fundamentals and everything to do with animal spirits. Or, maybe cocoa is the new sound money?

That’s it for this week.

Get rich or have fun trying.

Scroll down for a treasure trove of quantitative trading papers. Thanks Rob!

Past winners of the Charles H. Dow Award

*************

ICYMI: Post Nirvana

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.