Q1 2025 is looking rather binary.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Q1 2025 is looking rather binary.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Try Spectra School for free!

If you’re looking for a good way to spend 35 minutes or so, check out Lesson 3 of our flagship course “Think Like a Market Professional” for free. https://spectramarkets.com/lessons/tlmp3/ There, you will find the entirety of Lesson 3, for free, along with a link to my Learning From Legends video with Ben Hunt.

The lesson is called “Surfing the Narrative Cycle” and delves into how you can understand the stories the market is telling itself. If you like it, you can sign up for the full course and use coupon code LESSON3 for $250 off the $1200 price (i.e., you pay $950 for 16 lessons and 10+ videos.)

Happy Friday the 13th.

The USD keeps on ripping. Stocks keep on ripping. Crypto keeps on ripping. Everybody is getting rich! We continue to ride the soft landing wave as the Bigfoot recession (often spotted, never real!) will have to wait another year.

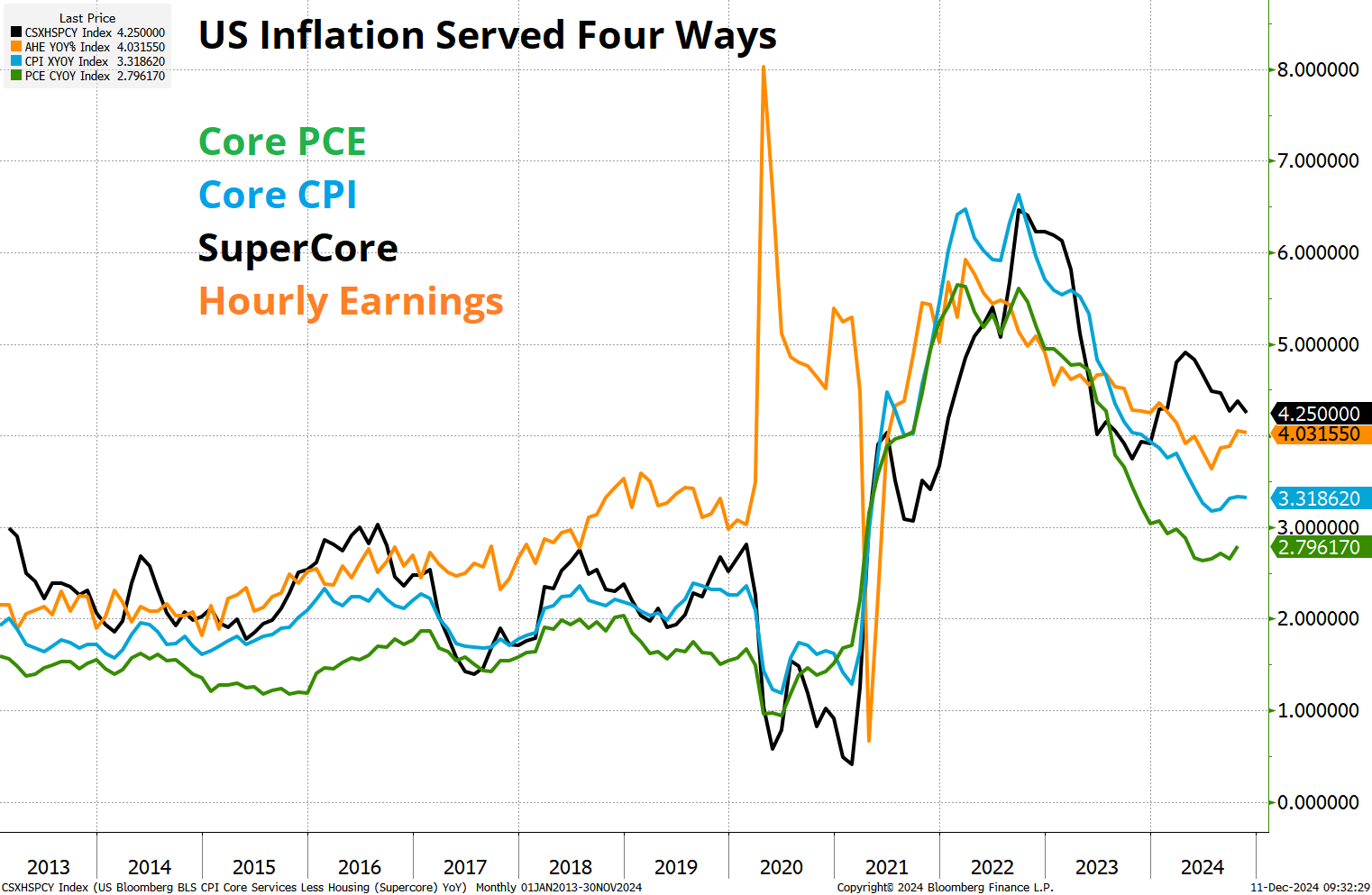

You can now add “sticky inflation” to the list of things that might cut us down to size in Q1 2025. CPI came out this week, and the inflation story in the US is not great as the “sticky inflation” scenario gains more credence with every report.

Headline, Core, Wages, Supercore, and inflation expectations all suggest that inflation has bottomed here—way above 2%. Core CPI is 3.3% and rising. Supercore and Average Hourly Earnings are above 4%. This is not mission accomplished, at all. This is pretty much the definition of sticky inflation.

There is a world where the Fed hikes zero times in 2025.

Those lines on that chart have been going sideways or mildly higher for months.

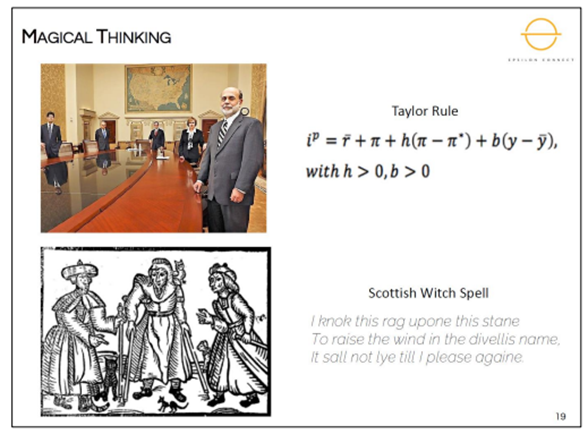

When it comes to monetary policy, nobody has a clue where the neutral rate is, so the longer inflation remains elevated and well above target, the higher policymakers will assume the neutral must be—and the fewer interest rate cuts we should expect. You’ve got 600 PhDs at the Fed watching CPI and PCE and the stock market and GDP and then glancing over at Fed Funds and coming up with this sort of observation:

Neutral is unobservable so the only way you can quasi-try-to-observe it is by comparing the evolution of Fed Funds to changes in financial conditions over time. The longer you keep rates up and financial conditions keep loosening, the higher your estimate of r* must be. But by the time you decide to raise your estimate of neutral, the past tightening will probably kick in, triggering a recession and a lower neutral rate going forward. Do you see how silly this is?

It brings to mind one of Ben Hunt’s slides from the first Epsilon Connect Conference:

I didn’t come here to say the Fed should replace some of its PhDs with witches from Scotland. I am simply saying that because nobody knows anything about how inflation or economics or monetary policy actually work, except in hindsight, we end up feeling our way through the darkness, guided by the beating heart of financial conditions. If nothing breaks, the Fed will assume neutral is higher than before, and they will stop cutting.

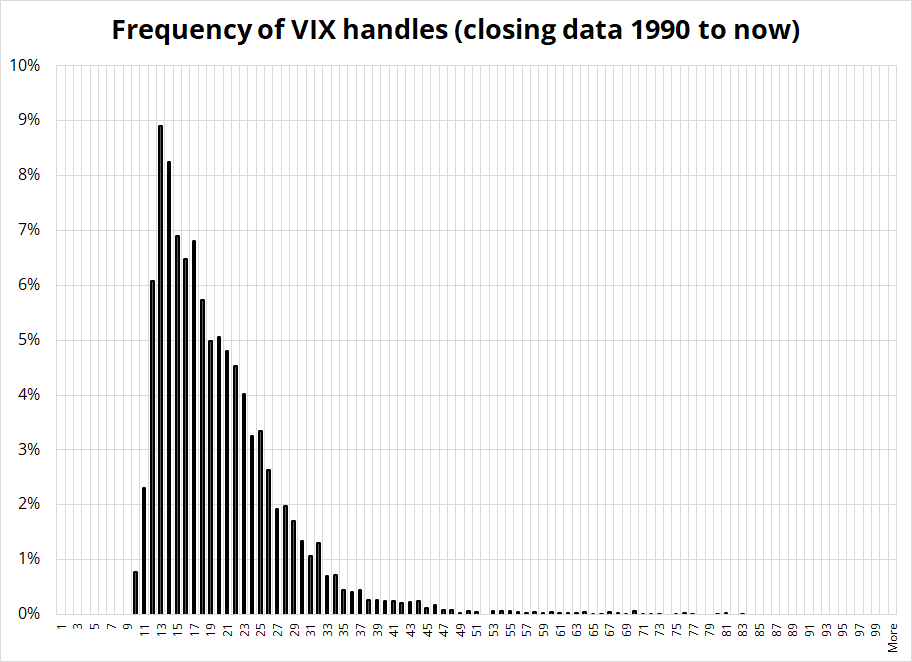

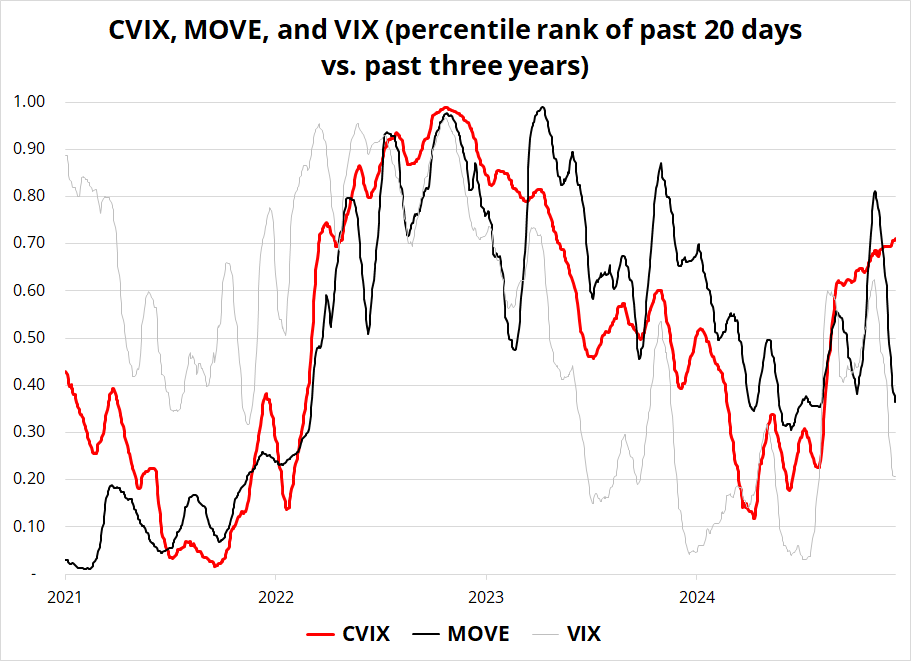

Remember the old theory early on in this cycle was that the Fed would hike until something breaks, because soft landings are impossible and the economy has to be in either bubbling boom or bitter bust. Reality, of course, says otherwise as the VIX spends more time on a 13 handle than any other.

82% of all days since 1990, the VIX closed below 25. Life is kind of boring a lot of the time! We are not always roller coaster riding from an overheated economy straight into full on depression. Sometimes we just glide along at 5% nominal growth for years at a time. That’s what is happening now.

And even though I think stocks will finally correct in Q1, I don’t expect a recession in the USA because balance sheets remain super strong and all the leverage in the system is in financial markets, not the economy. So the US could experience a major correction or bear market without much damage to the real economy.

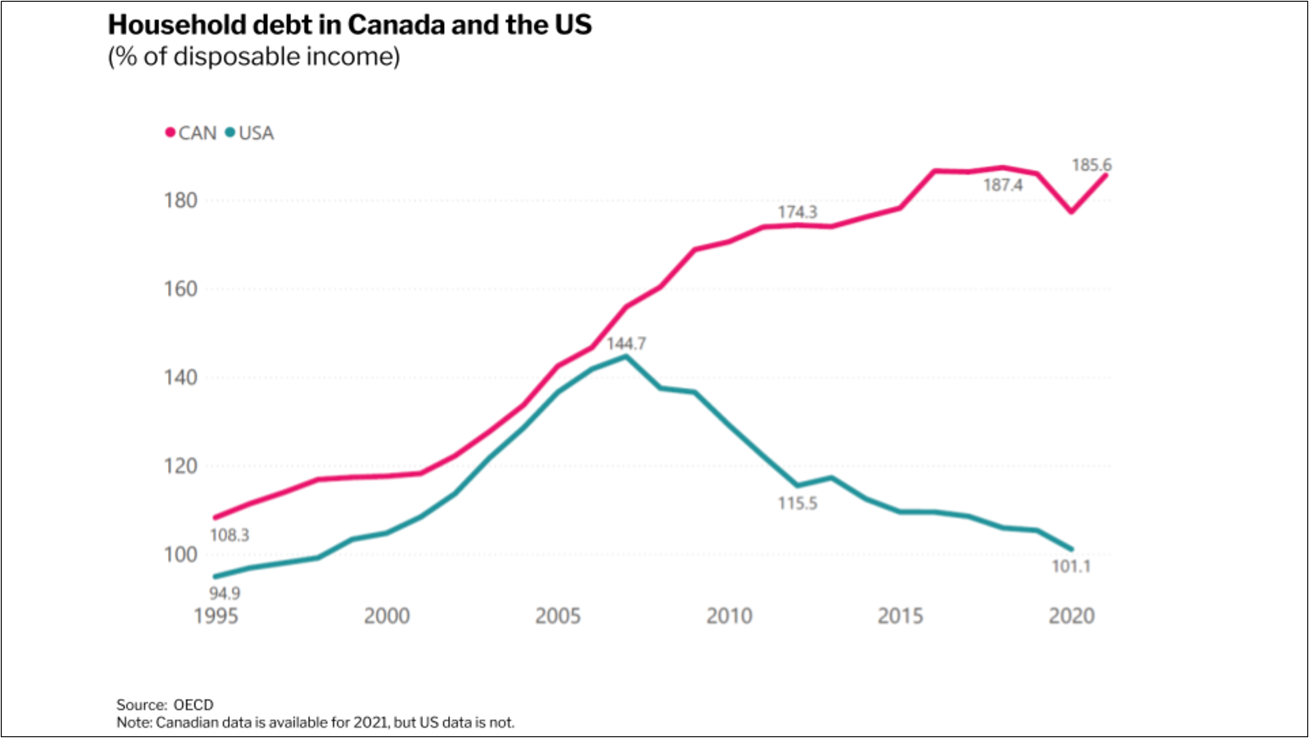

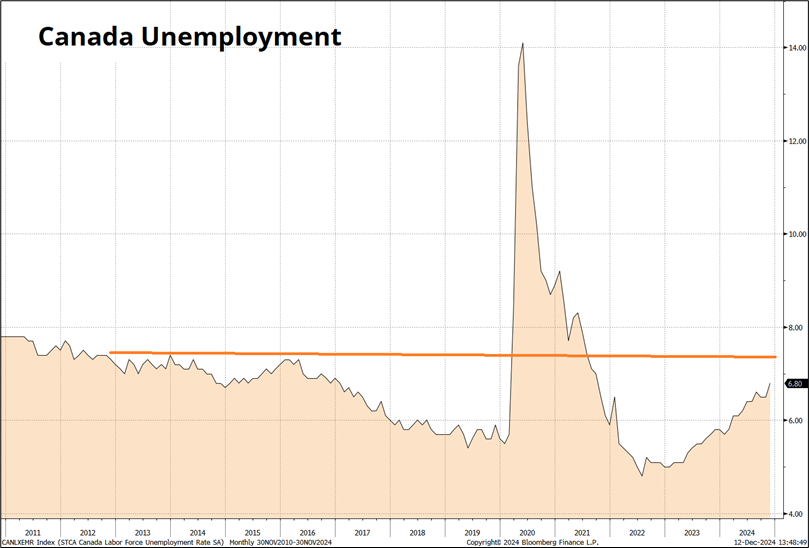

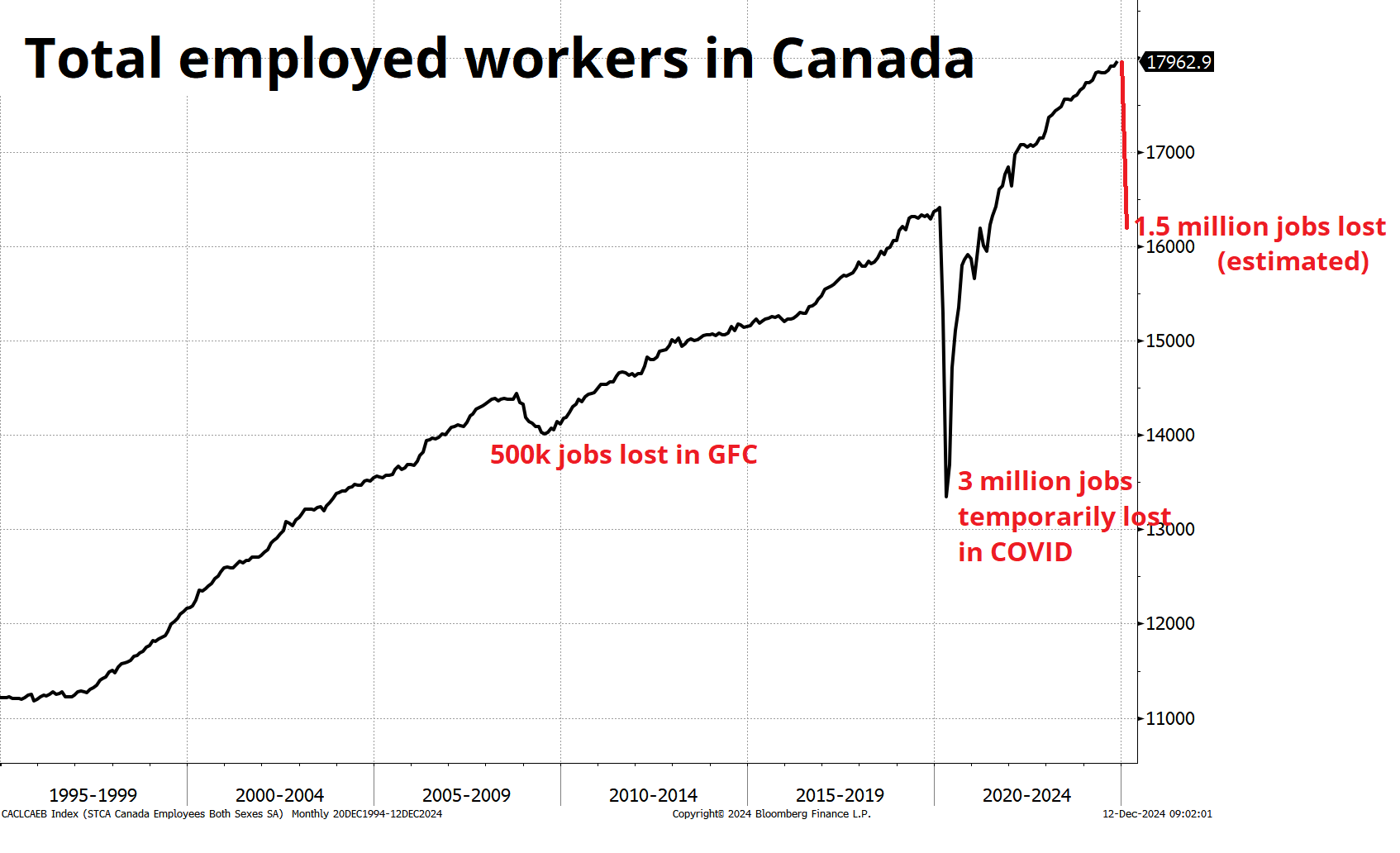

In other countries (like Canada) this is not the case. Consumers are megastretched up North, balance sheets are fragile, and the chickens that came home to roost in the USA in 2008 just kept on bobbing and cluck clucking around Canada for another 16 years.

This chart is not a good bearish Canada thesis. It’s been around for 10+ years. But I have always said that when people start to lose their jobs in Canada, this debt overhang going to matter. And now that’s starting to happen as Canadian Unemployment dribbles higher.

Editor’s note: Yes, things mostly dribble lower, not higher. But imagine a spaceman in the International Space Station drinking apple juice and some spills out of his mouth and there is no gravity so the juice dribbles higher. You with me?

You can see by the horizontal line that we are still below peak unemployment levels reached in Canada in 2012/2016 – and there was no cataclysm at that time. But pressure is building in the Great White North as Trump threatens tariffs, GDP growth is weak, immigration will stop contributing, and debt is voluminous.

The US is antifragile, Canada is not.

Don’t forget to buy the 2025 Spectra Markets Trader Handbook and Almanac here.

If you trade MSTR or PLTR, you might find this excerpt from am/FX of some use.

—

James Seyffart of Bloomberg wrote an outstanding piece predicting MSTR will be added to the NASDAQ 100 this week. The announcement of the NASDAQ 100 add/delete plan comes out this Friday after the close, and the effective date will be December 23, which means the indexers need to complete their buying by the close on December 20. Check out the article here, there is so much detail—it’s an incredibly professional and expert writeup.

Index inclusion is an interesting, controlled experiment for the efficient markets hypothesis because everybody knows about the adds/deletes beforehand now, whereas in say, 2000, it was kind of niche knowledge. See this crazy trading story from the year 2000, for example, when you have 8 free minutes.

Anyway, the idea that stocks benefit from inclusion in indexes as passive buyers are forced to purchase yards of stock at any price doesn’t work anymore. It has been arbitraged away over the years as the market front runs the add/delete and then when it actually happens, market maker and speculative positioning is equal to or sometimes larger than the required buys from the indexers.

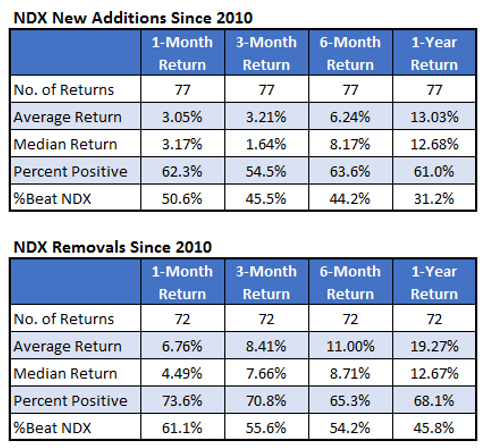

This excellent writeup (Removed NDX Stocks Likely to Outperform Those Added) features a table which is consistent with studies I have seen of S&P add/deletes.

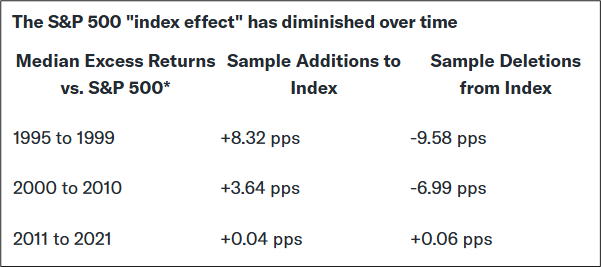

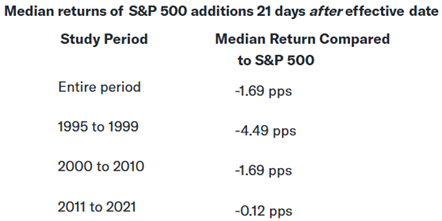

While that study covers the period from 2010 to now, another study done by S&P Global looked at the evolution of returns for S&P 500 additions and deletions over the decades. The output shows the returns during the period from the announcement date to the actual addition (around two weeks).

So the old pattern was that the stocks rallied into the addition. But that doesn’t happen anymore because analysts are pretty good at predicting which stocks are going to be added to various indexes (e.g., that article about MSTR I linked at the start). And everyone gets ahead of the flow. Anyone that gets long on the announcement knows that by the time addition day hits, the whole thing is priced in… So they get out early. On the flipside, there used to be a selloff after the additions, because the stock would get ramped on add day (e.g., my article about trading JDSU in the year 2000).

Again, the effect disappears over time. This is a classic example of high Sharpe trades slowly decaying towards a terminal Sharpe of zero. When there are French fries scattered in the Walmart parking lot, a few birds will notice them at first and those birds will fly down and get fat and be happy. Then, quickly, many other birds will swoop in to peck at the minimal salty remains until there is nothing left to peck at.

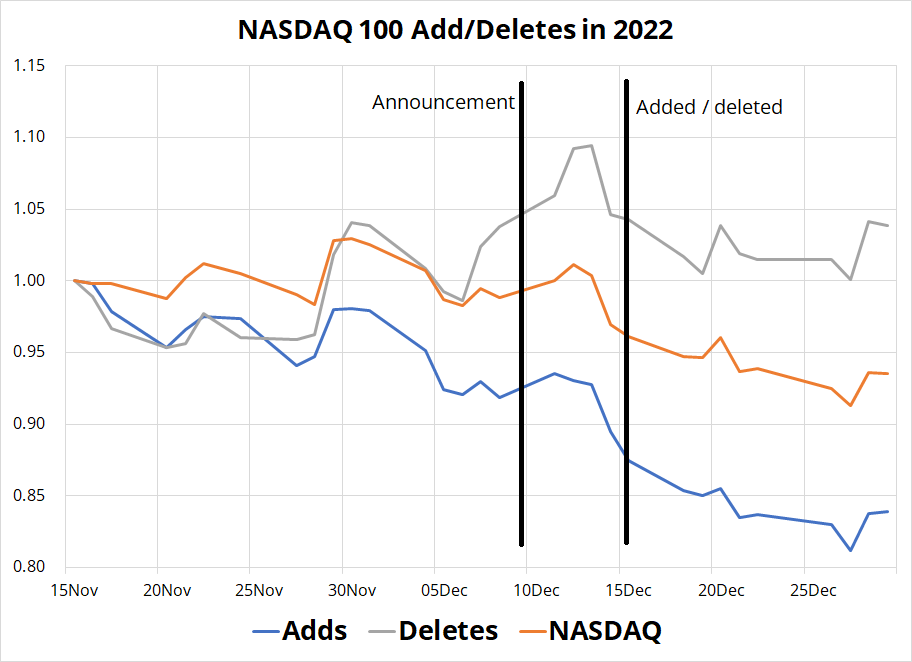

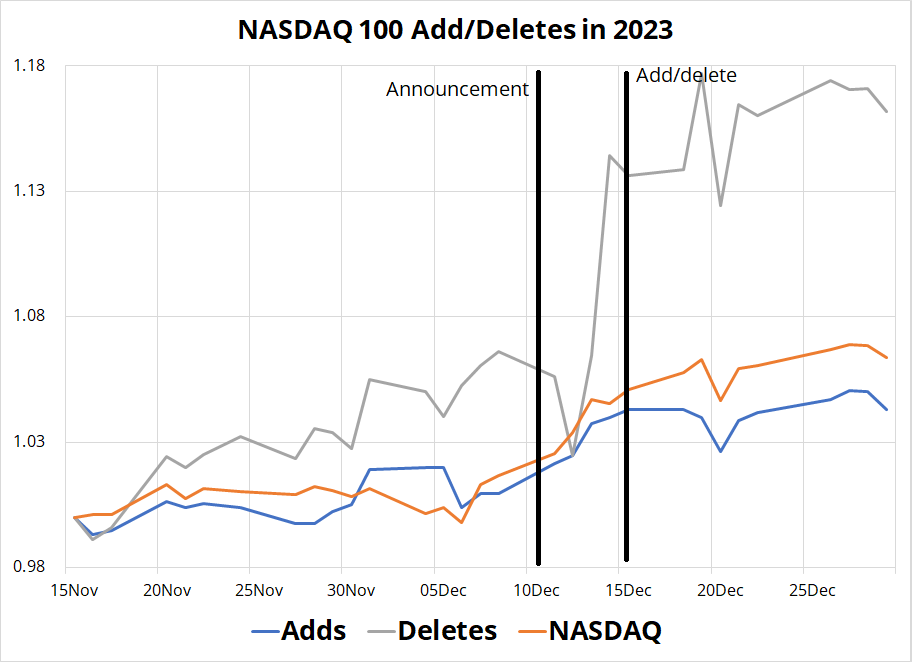

Out of curiosity, I looked at 2022 and 2023 to see what specifically happened each year. Here are the charts.

You can see in both charts that the adds showed negative performance vs. both the NASDAQ itself, and the deleted stocks, in one bear and one bull period. There was a little bump up around the announcement date both years, but not much else to chew on. Selling the adds to buy the deletes is the surprising winner both years.

Perhaps the most interesting scenario this year would be if MSTR does not get added to the NASDAQ because they rule it to be a financial stock not a technology stock (like Coinbase). This would be the correct ruling, in my view, as Saylor’s software business is an unprofitable, de minimis contributor to the stock and company performance. That said, I don’t think the ICB reads am/FX, so my opinion is probably not important.

—

End of excerpt—so that’s the deal with the add/deletes. They’re a fade, not a go with.

Despite some wild up and down days, the NASDAQ and SPX are close to unchanged this week, and the VIX remains on its favoritest handle: 13.

It is mildly interesting that despite new all-time highs in the indexes, NVDA is showing considerable relative weakness over the past 30 days or so.

This week’s 14-word stock market summary:

Fed is no longer a tailwind, but nobody sells until the new tax year!

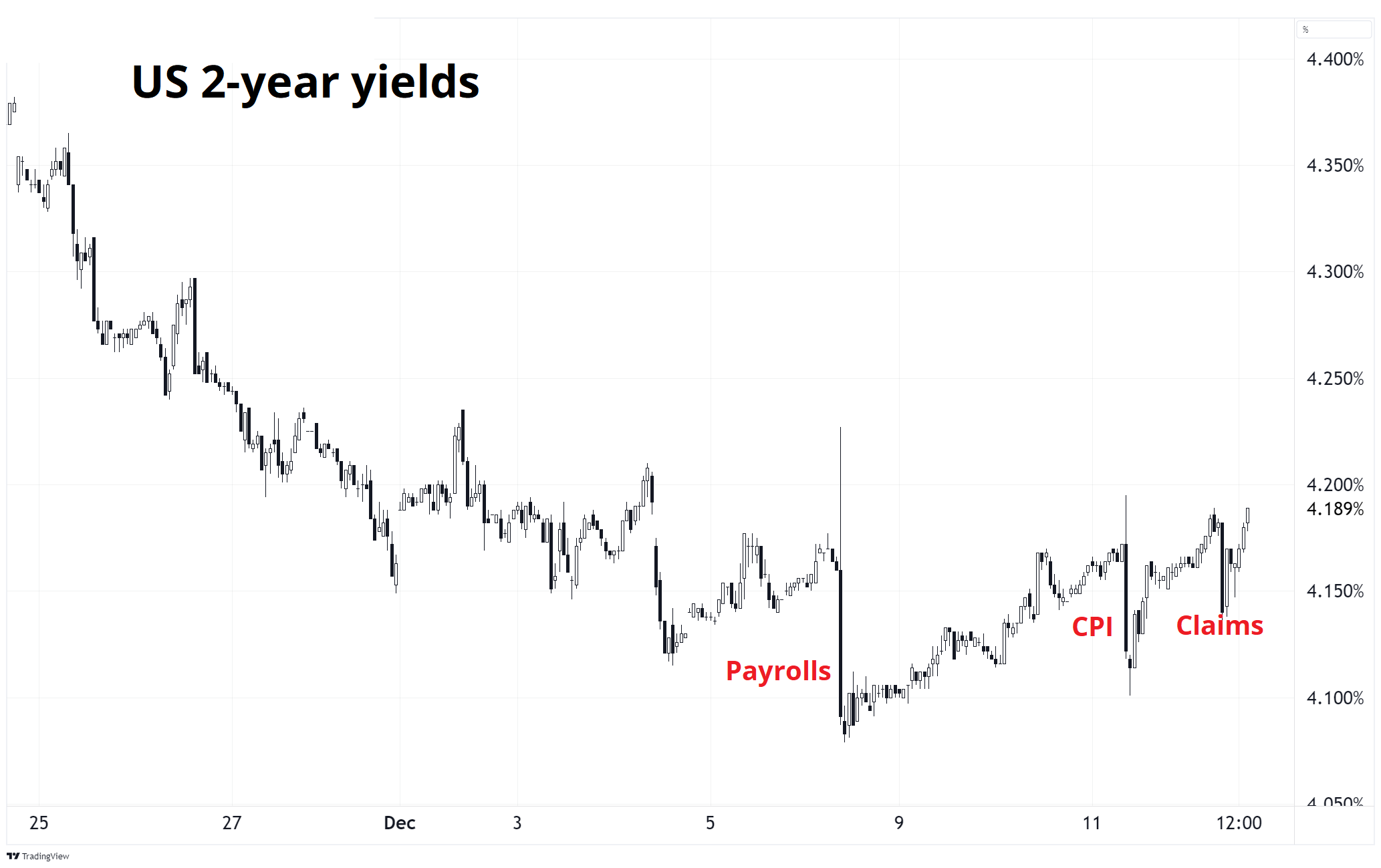

The US 2-year yield is imitating a beach ball under water as NFP, CPI, and Initial Claims data all tried to submerge it, but it snapped back higher thrice.

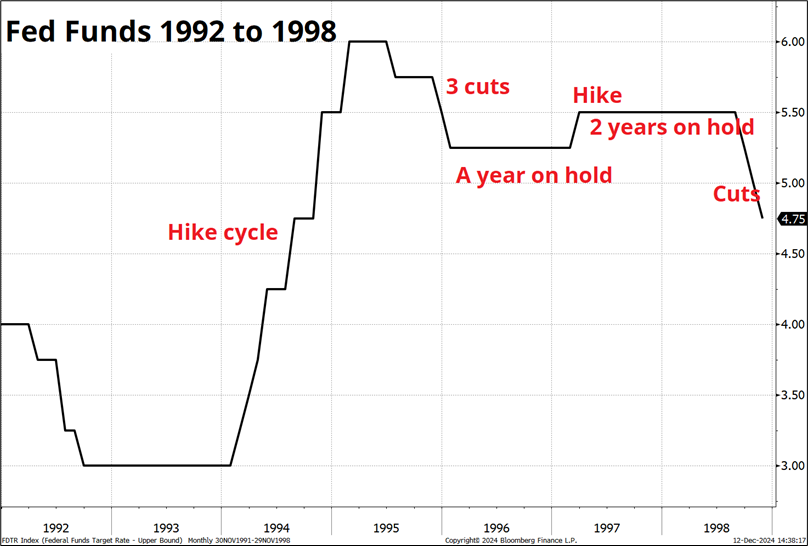

I think that yields have sniffed out the fact that inflation remains way too sticky and further Fed cuts are not justified. The FOMC will cut next week just because it’s priced in, but then you can be open to the idea that there might not be another Fed cut for a long time. A small mid-cycle adjustment like this is not unheard of. It happened in the late 1990s.

There are enough similarities between the 1995 soft landing and the 2023/2024/2025 soft landing to think that “Fed on hold for all of 2025” is a scenario worth considering, if not the base case.

Elsewhere around the world, the ECB cut 25 as expected, the Bank of Canada cut 50 as expected, and the Swiss National Bank cut 50bps as expected by some people, but not by me. The currency didn’t respond much, and the SNB remains trapped in a situation similar to the one faced by the Bank of Japan before Abenomics: Strong currency + low inflation + no credible weapons.

The USD is stuck in this weird nonequilibrium where we are on hold, waiting for accurate information on tariffs. If the tariffs come in bigly, the USD is too cheap, and if the tariffs are measly or nonexistent, the USD is too expensive. Choose your own adventure.

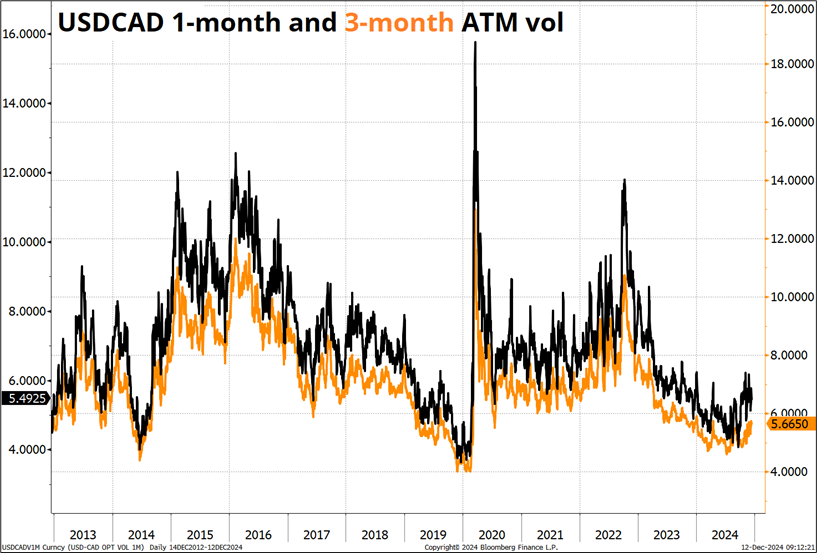

While tariffs are clearly bullish USD, their impact on stocks and bonds is less obvious and that is probably why FX volatility remains bid while equity and fixed income vol are circling the bowl.

I continue to believe that the Canadian dollar market is way too complacent about tariffs in early 2025.

I have been trying to figure out the Canada angle as we are just 39 days from inauguration and USDCAD is either 200 points too high or 400 points too low. A 25% tariff on all Canadian goods would be so damaging that it’s almost impossible to handicap where USDCAD might go if it came to be. After setting it up, it seems too weak for Trump to then simply back down without first inflicting some sort of psychic pain on Canada. Maybe he does the 25% tariff on Day One and all hell breaks loose and they quickly negotiate some sort of deal that involves tighter border controls and such? That would be quite the ride for USDCAD in January. 1.42 to 1.46 to 1.40 in one month.

Sometimes I type things like that and think I’m being hyperbolic but this really seems like a time where a bigger imagination is less risky than too small of an imagination. My alma mater wrote up a short piece here which suggests that a 25% tariff would lead to 1.5 million job losses and a GDP reduction “significantly greater than 2.4%” for Canada.

I suppose the easiest thing is to simply assume Trump is bluffing and not worry about any of this, but it’s certainly not a zero probability that these tariffs get announced on Day One, and the negative employment impact would be 3X the impact of the GFC or 0.5X the impact of COVID.

Can we even say that the base case is that he’s bluffing? The base case is probably smaller tariffs on Day One with the threat of scaling increases over time. This gives Trump the power to push allies around without actually blowing a huge hole in the US economy. Bessent and Musk have both spoken about the need for gradualism on implementation, while Trump does not want a repeat of 2016/2017. He wants quicker results this time.

Meanwhile, here’s USDCAD volatility. The market is just not taking any of this Trump stuff seriously, at all. They probably should!

USDCAD to 1.45 by January/February seems reasonable.

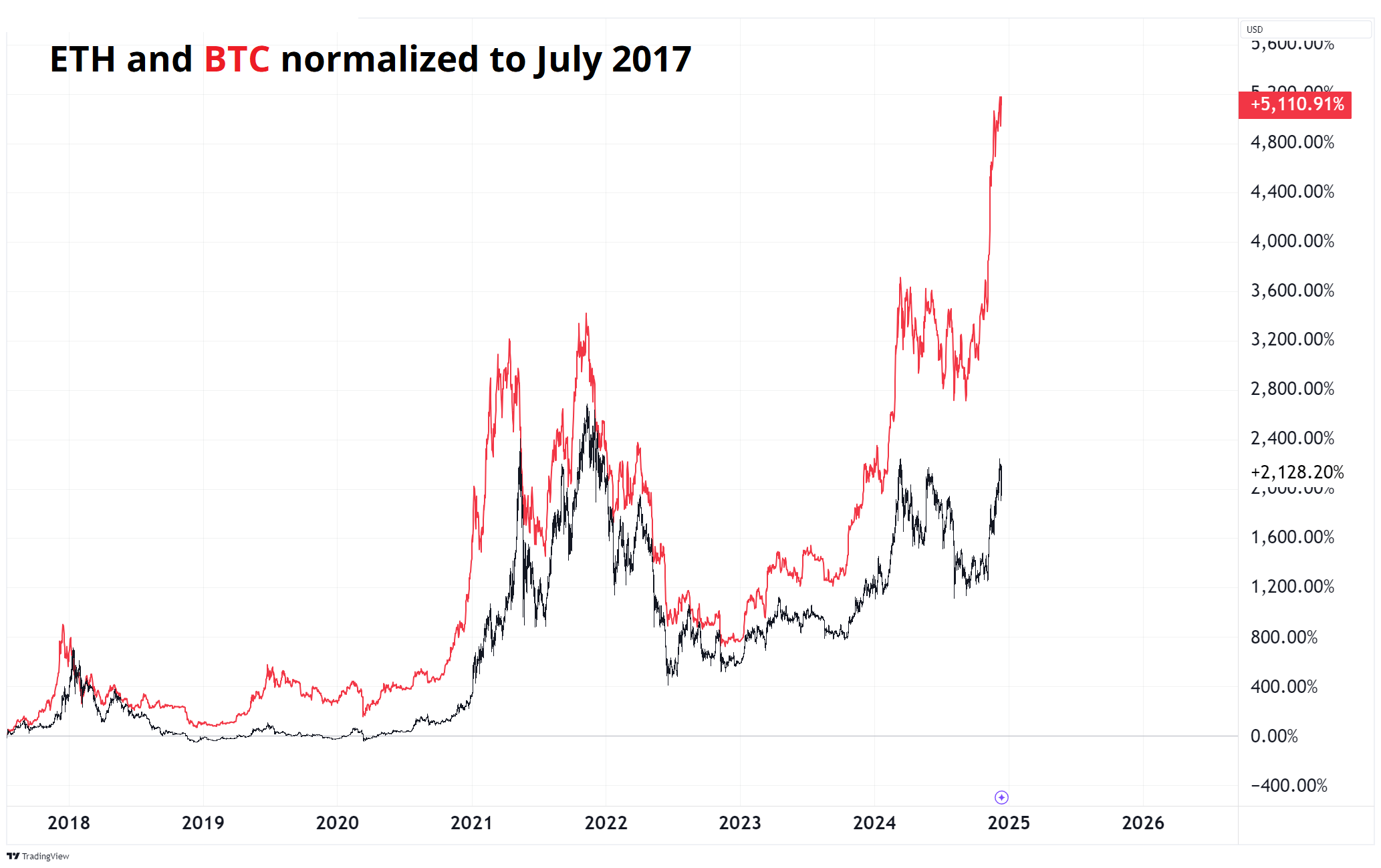

Bitcoin is consolidating as it oscillates back and forth between five and six digits. Meanwhile, MSTR and friends have stabilized, but not pulled back much. ETH has awoken from its slumber, though it has not even taken out the late 2021 highs as there are 100s if not 1000s of competitors to ETH, with SOL particularly taking large chunks of attentional and transaction market share from ETH.

You can see how BTC ripped through those 70k highs as it went to 100k, while ETH, which hit 4800 in 2021, is just shy of 3900 as I type this. It used to be the high beta until SOL and other favey faves showed up. BERT, WIF, and PNUT are way more fun than stodgy old ETH. Vitalik must be, like, 50 years old or something by now. For crypto natives, trading ETH is like trading IBM.

There’s a ton going on in individual ags and other pockets of commodity world, but the behemoths are boring. Gold and oil are just chopping broccoli right now. Silver continues to offer hilarity, but not profits. Imma cut Friday Speedrun off right here because this is getting longer than usual.

That was 11.354 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

FT: A guide to 2025 investment outlooks by someone who hasn’t read them.

This is one of the funniest financial articles I have read in ages.

A fantastic learning opportunity

Aswath Damodaran offers a free chance to learn.

Scott Aronson discusses Google’s Willow quantum chip

A breakthrough that will eventually reshape the world.

Linkin Park live in Grand Central

Might bring you to tears of joy and sadness.

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.