The USD down trade isn’t working but it’s also not really not working. Welcome to the 2024 stretch run!

US Route 50 covers 3,000 miles from CA to MD

Image source: Wikimedia Commons

The USD down trade isn’t working but it’s also not really not working. Welcome to the 2024 stretch run!

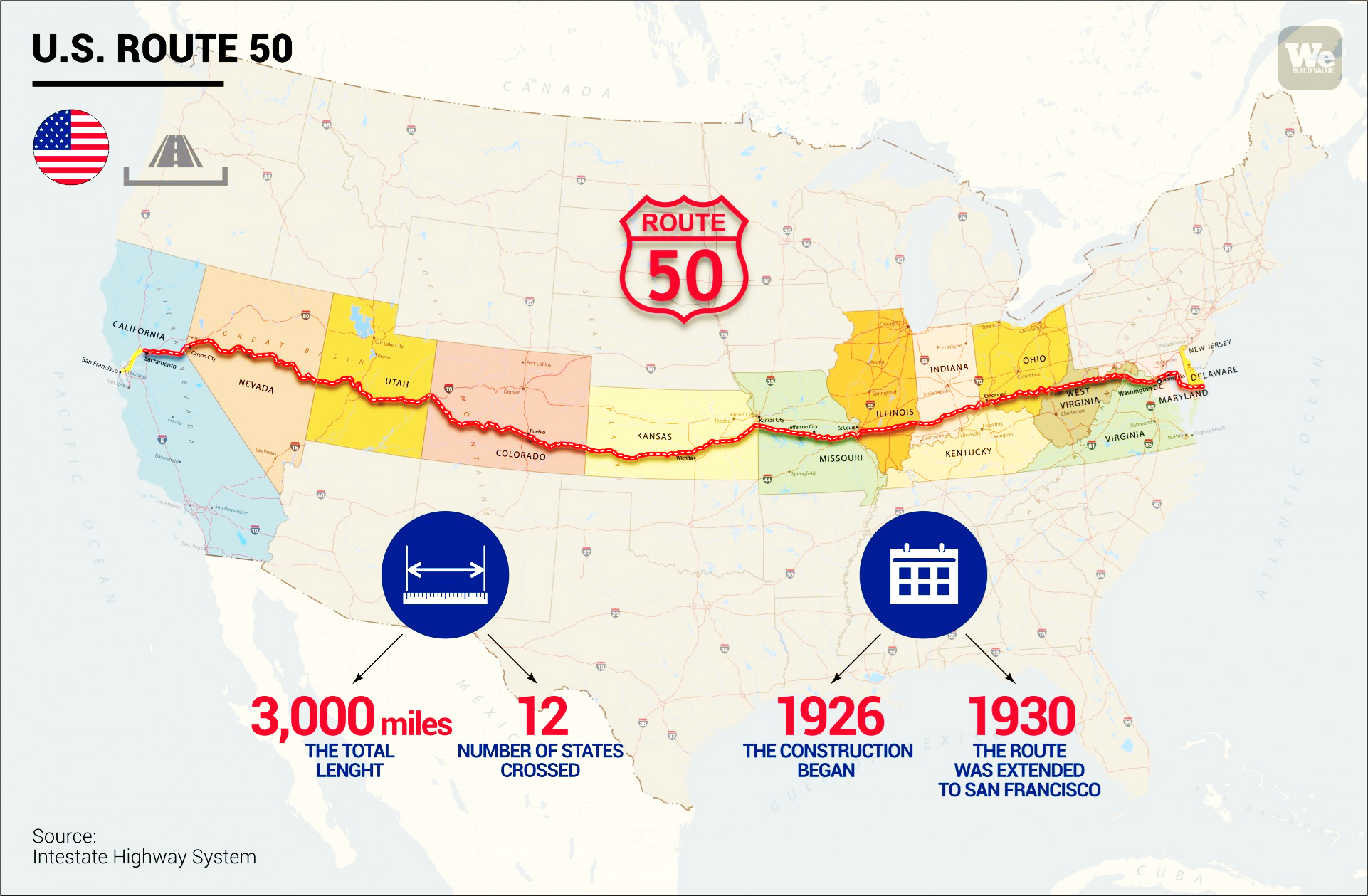

US Route 50 covers 3,000 miles from CA to MD

Image source: Wikimedia Commons

Long 06SEP 0.6100 NZD put

for around 28 USD pips off 0.6150 spot

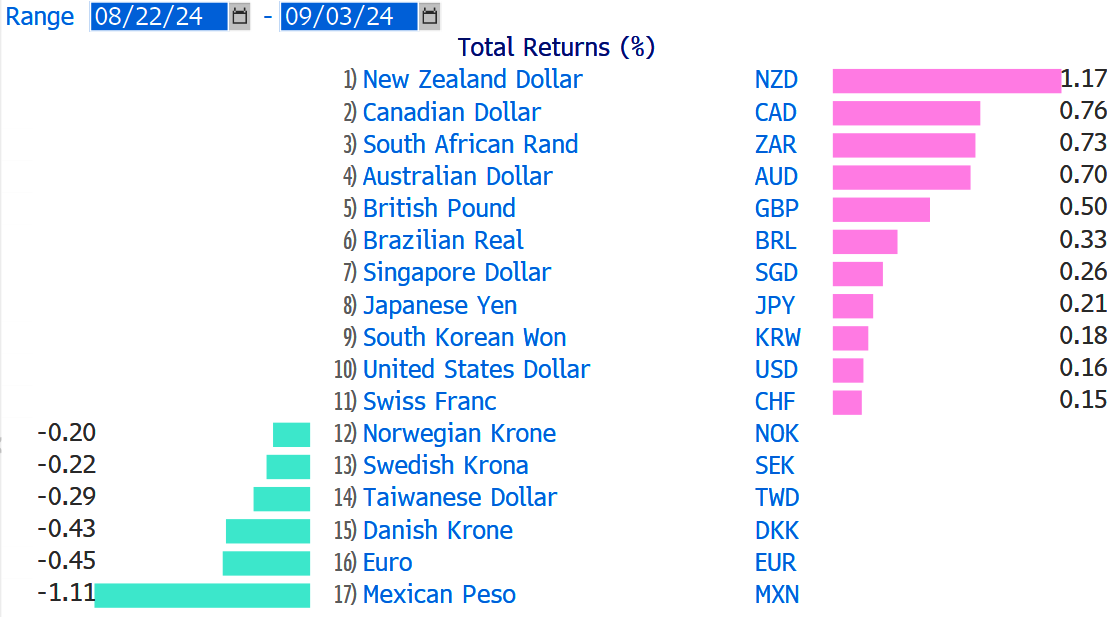

Welcome to week 36 of 2024! After playing short-handed for most of the past two months, the markets are back to full strength and gearing up for the stretch run towards the 31DEC finish line[1]. When I left for Canada on 23AUG, I was skeptical of the USD selloff and while it has not followed through, there have been pockets of weird USD weakness and USD strength scattered somewhat randomly. To wit:

FX changes since August 22

Elsewhere, the AI story still looks very tired to me, but despite post-earnings weakness, NVDA is still much, much closer to the all-time highs than the YTD lows. Once the narrative in a stock like NVDA turns, the price can lag but tends to eventually catch down to the exhausted narrative.

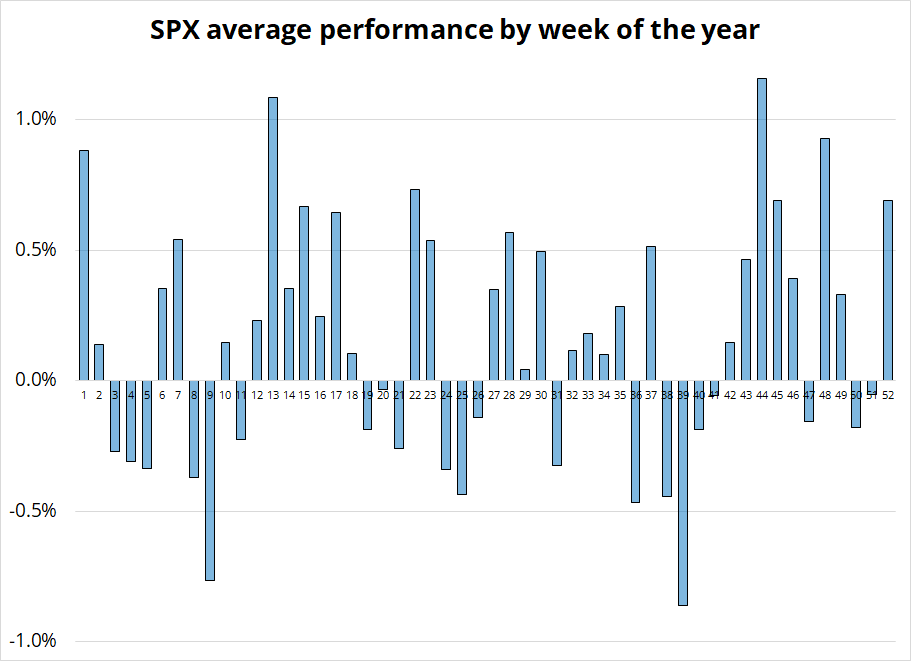

Speaking of stocks: We are now entering a bad period for equities as average returns for weeks 36, 38, 39, 40 and 41 are negative as you can see in the chart below. Only 21 out of 52 weeks exhibit negative average returns, so to see five of them clustered into a six-week period is worthy of a bit of a fear factor. I am using data from 2000 to now for this weekly performance analysis.

The overall setup doesn’t look particularly attractive for risky assets to me because:

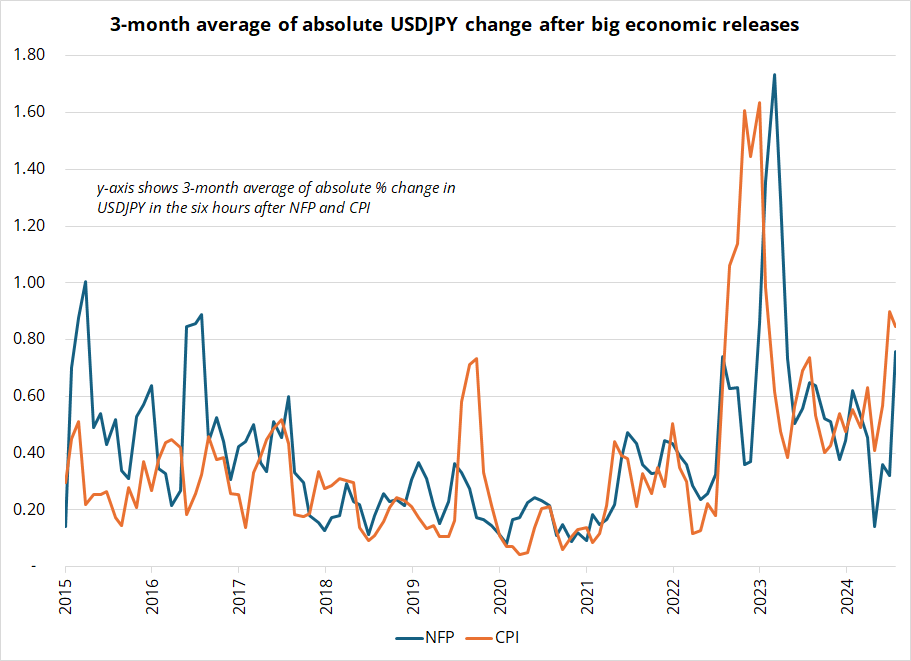

Speaking of NFP, note that common knowledge now says that we have transitioned from a regime where CPI is the most important data release to one where NFP is the big dawg.

That said, recent data suggest both releases are still having similar market impact. This next chart shows the absolute % change in USJDPY after NFP and CPI (3-month average). You can see that CPI mattered more in 2022, then there were some huge NFPs in early 2023, but both have had decent market reactions of late as the July CPI and August NFP both uncorked 1.5-percent USDJPY moves.

My guess is that the common knowledge will be correct, and CPI will lose importance relative to NFP over time as the inflation shock of 2020/2023 is history and the Fed doesn’t really care much about the difference between 2.0% or 2.6% or 2.9% inflation.

—

[1] I mix horse racing and hockey metaphors like a boss.

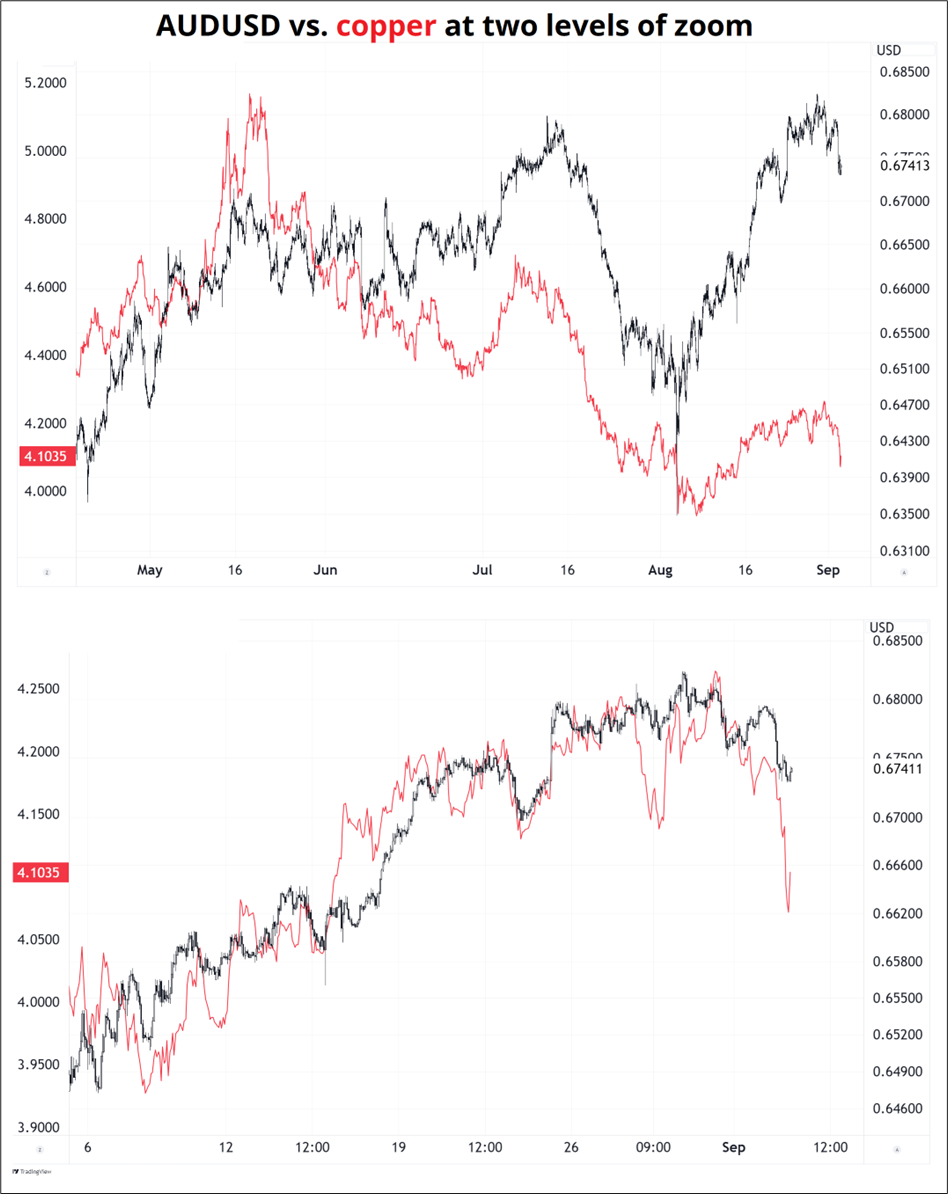

AUD, NZD, and CAD look quite high relative to copper as you can see here (using AUD).

Finally, we have a pretty wicked calendar this week, with double ISM, Bank of Canada, NFP, and perhaps most notably: Waller gives a speech on the economic outlook at Notre Dame (with Q&A) on Friday at 11:00 a.m. NY. This comes 150 minutes after payrolls and could be spicy timing. Waller is always a key figure to follow, despite the red herrings he has been dropping since he suggested rate cuts were maybe 3 or 4 months away back in November 2023. He is at least the best representation of the Fed’s mark-to-market. Their guidance these days is more like reval to spot economic data, not forward looking policy direction.

Thank you for subscribing to am/FX and for trading with Spectra. You are appreciated.

I hope your P&L moves into high gear over the next four months.

Route 50 covers 3,000 miles from CA to MD.

https://www.webuildvalue.com/en/reportage/us-highway-50.html

{kind=link}