While core inflation continues its slow descent, headline has been sticky, but should be set to fall now as oil, gasoline, lumber, and used car prices fall.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

The most important CPI release since Christopher Columbus “discovered” North America delivered a happy outcome as inflation continues to drift lower. Inflation does not fall like a rock; it falls like one of those awesome helicoptering maple seeds in fall.

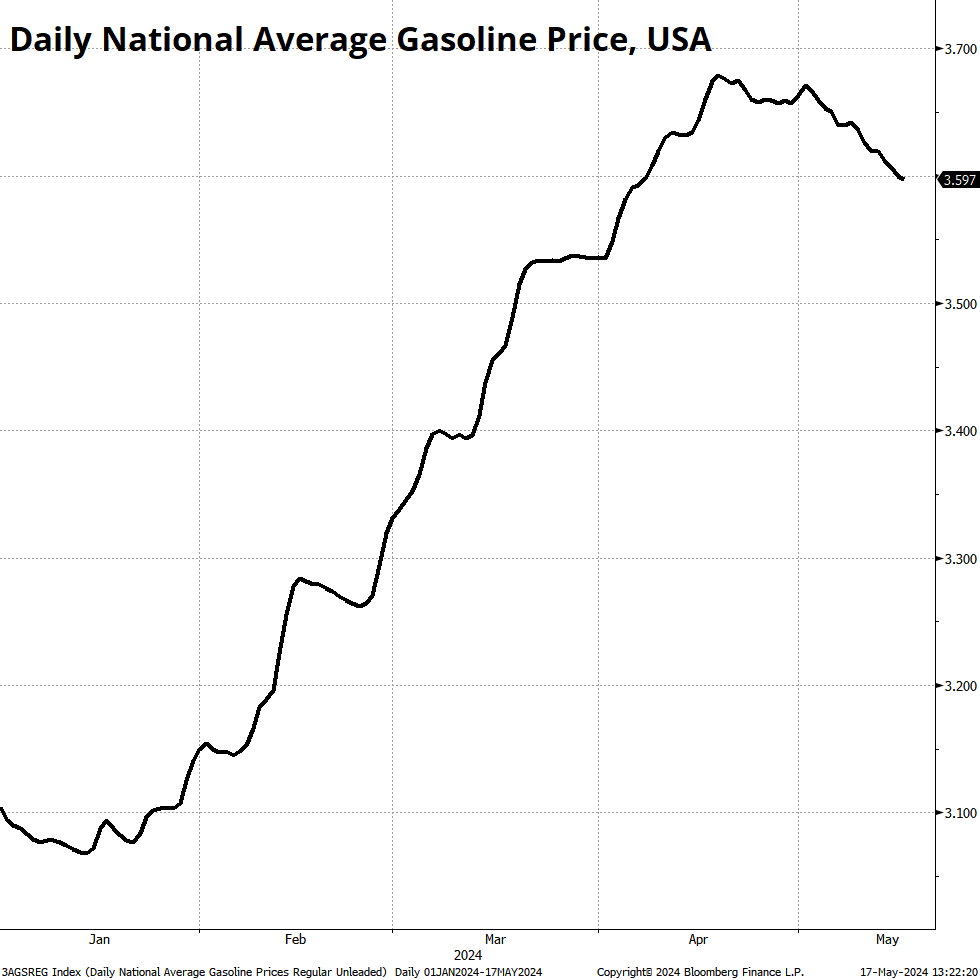

The falling maple seed takes a long time to get to the ground, but it generally gets there, even if gusty winds and updrafts might push it temporarily up on the way down. While core inflation continues its slow descent, headline has been sticky, but should be set to fall now as oil, gasoline, lumber, and used car prices fall. Here, for example, is the price that most impacts American inflationary psychology: The price to fill up your Ford F-150.

It is not written in the stars that gas prices will continue to go lower, but we are more than halfway through May, so it’s increasingly written in the stars that the energy contribution to CPI this month will be negative. Still, with 25 or 55 different inflation series to choose from, one can easily argue that inflation is still a huge problem, or that inflation has been completely vanquished. The truth is somewhere in the middle.

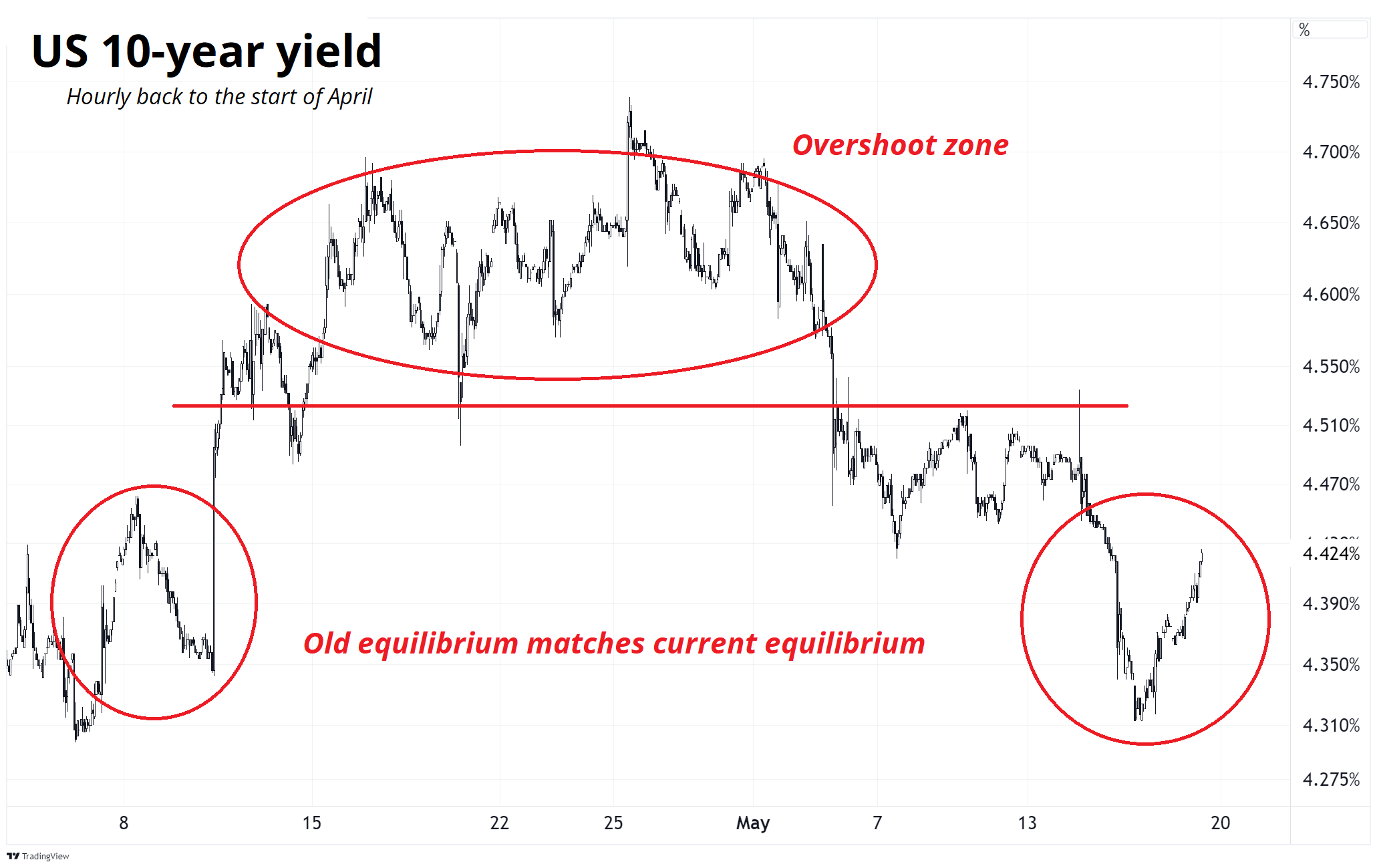

The weakening US data has been a theme for a few weeks now, and we got more whiffy hard data as housing and Retail Sales missed expectations this week. The market has now fully embraced the idea that US economic data is no longer pinned to the red line, but the jury is out as to whether this is a mini soft patch or the start of something more nefarious.

One of the big economic data analysis issues of the current millennium is that there are simply way too many data points to look at. This leads to a huge confirmation bias problem because if the mainstream economic data isn’t supporting your worldview, you can simply look under the hood at more designer indicators and utter smart-sounding platitudes like:

The devil is in the details.

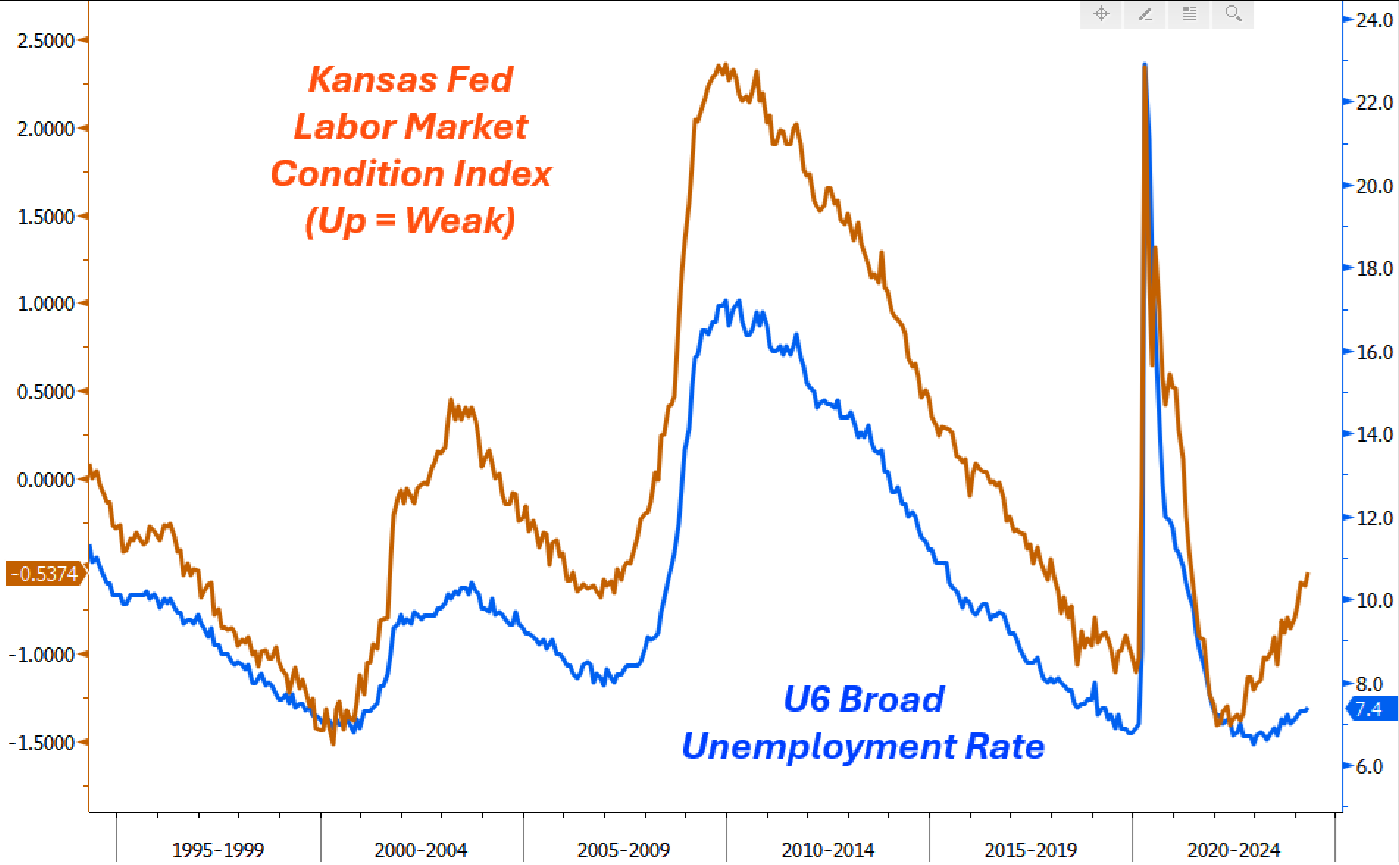

That’s why I like this chart from Macro Alf. It takes the average of 24 job market indicators in the USA to avoid the cherry-picking problem, and compares them to the unemployment rate.

The more broadly cited unemployment rate (U3) is currently at 3.9% and looks like it’s headed to the 4.2%/4.4% area soon. That will be enough to trigger the Sahm Rule and ratchet up recession fears and US rate cut hopes.

Alf and I talk much more about that chart in this week’s podcast. The podcast is not Roganesque. It’s always just ~35 minutes long.

Outside the US, the market keeps looking for a dovish Bank of England and more rate cuts from the ECB, but those stories are getting stale, and it’s been very difficult to price in more than three cuts for the ECB. While Lagarde et amis have promised a June 6 cut, any cuts after that are going to depend on the data.

Finally, China announced a partial bailout for their residential property sector and opinions vary on whether or not it matters. Some say it’s exactly the right way to assist in a balance sheet recession while others say it’s small potatoes and could serve to exacerbate Chinese real estate woes by buying homes below market and forcing prices even lower. There is no coherent narrative on China, just a bunch of divergent opinions.

Stocks

Stocks are in wood chopper mode as softer US data takes the pressure off the Fed and puts us back into the Goldilocks regime where you can say “solid nominal growth” and “The Fed is gonna cut” in the same sentence without sounding bananas. Fed interest rate cuts in a solid economy are what equity bull dreams are made of.

The three major US indices made new all-time highs this week with the SPX, DJIA, and NASDAQ all touching levels not seen since ever. While sentiment is overwhelmingly bullish, that’s always the case during bull markets.

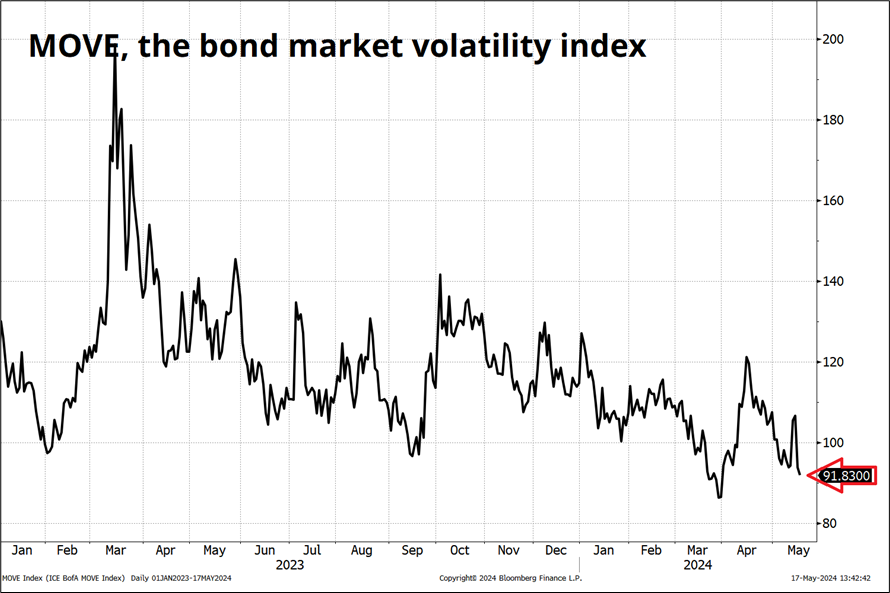

Stocks are said to climb a wall of worry, but strangely I don’t even know what to worry about right now? Recession? Maybe, I guess? Overheating? Nope. Middle East? Not really. Corporate earnings? Nope. Bond market volatility? No sir/madam.